Learn how an FHA loan calculator prevents budget disasters. Step-by-step tutorial to estimate monthly costs and find your true price range before shopping.

Introduction: The $500 Monthly Mistake

You fall in love with a house. The kitchen is perfect. The backyard is huge. You sign the offer. Then the first mortgage payment arrives — and it is $500 more than you expected. That sinking feeling in your stomach? That is a costly mistake that thousands of buyers make every single year.

They forget to calculate the full cost.

A mortgage is not just the price of the house divided by 30 years. You have interest, property taxes, homeowners insurance, and the big one for FHA buyers: mortgage insurance. Guessing these numbers is dangerous. It leads to heartbreak, financial stress, and sometimes foreclosure.

But there is a brilliant tool that solves this problem before you ever step foot in an open house. It is called an FHA loan calculator, and it might be the most powerful weapon in your homebuying arsenal.

In this guide, I will walk you through exactly how to use an FHA loan calculator to set a realistic budget. We will cover every input field, break down every output number, and run real-world examples. By the end, you will know your true price range down to the dollar.

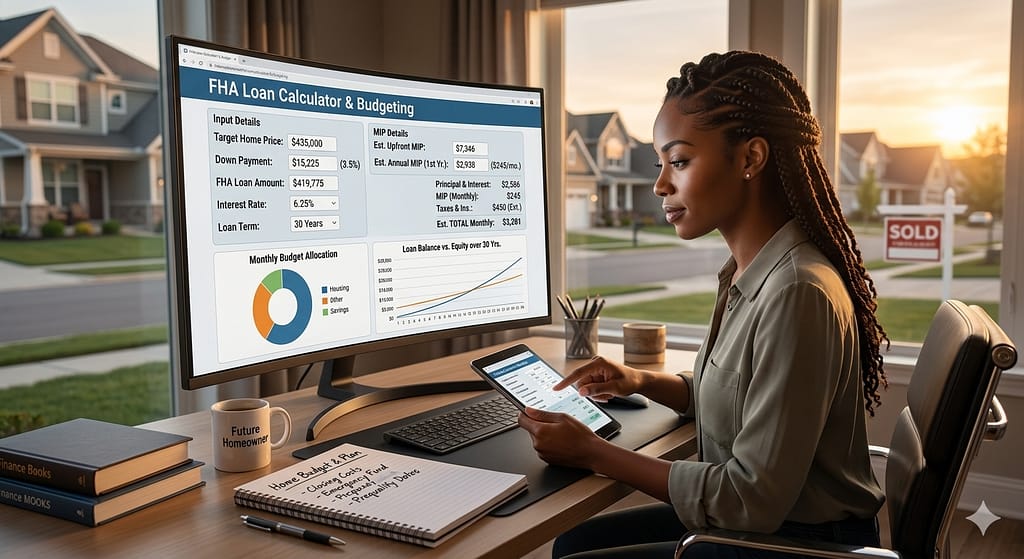

What Exactly is an FHA Loan Calculator?

An FHA loan calculator is a specialized financial tool designed specifically for government-backed FHA mortgages. Unlike a generic mortgage calculator, this tool accounts for the unique costs of an FHA loan: upfront mortgage insurance premium (UFMIP), annual MIP, and the low 3.5% down payment structure.

Think of it as a crystal ball for your monthly payment. You type in a few numbers — home price, down payment, interest rate — and the FHA loan calculator tells you exactly what you will pay every month for the next 30 years.

But here is the secret most real estate agents will not tell you: You should use this tool before you talk to a lender. Why? Because knowledge is leverage. When you walk into a bank already knowing your numbers, you sound like a serious buyer. You ask better questions. You avoid being sold a loan you cannot afford.

Why You Cannot Trust a Generic Mortgage Calculator

Generic mortgage calculators are everywhere. Bankrate has one. Zillow has one. Realtor.com has one. They are fine for rough estimates. But they miss two critical components of an FHA loan.

First, generic calculators ignore upfront MIP. An FHA loan charges 1.75% of the loan amount upfront. On a 300,000loan,thatis300,000loan,thatis5,250. Most generic calculators pretend this cost does not exist. An FHA loan calculator rolls it into your loan balance automatically, giving you a realistic total.

Second, generic calculators mishandle monthly MIP. Conventional loans use Private Mortgage Insurance (PMI), which eventually drops off. FHA loans use MIP, which often lasts the life of the loan. The rates are different. A dedicated FHA loan calculator uses the correct FHA MIP rates (0.45% to 1.05% depending on your down payment and loan term).

Using the wrong calculator is like using a map of New York to navigate Los Angeles. You will end up lost.

The Anatomy of an FHA Loan Calculator

Before we run examples, let us break down every input box you will see on a quality FHA loan calculator

Input Field 1: Home Price

This is the sale price of the house you want to buy. Be honest here. Do not type in the maximum a lender approved you for. Type in what you want to spend.

Input Field 2: Down Payment

For an FHA loan, the minimum is 3.5% if your credit score is 580 or higher. You can put more down — 5%, 10%, even 20% — but most people use this tool to test the minimum. The FHA loan calculator will show you exactly how a larger down payment lowers your monthly bill.

Input Field 3: Interest Rate

Rates change daily. As of this writing, FHA rates are roughly 0.25% to 0.5% lower than conventional rates. Check Freddie Mac’s weekly rate survey for current averages. Always open that link in a new tab for the latest data.

Input Field 4: Loan Term

Almost everyone chooses 30 years. It gives the lowest monthly payment. Some choose 15 years to save on interest, but your monthly payment jumps significantly.

Input Field 5: Property Tax Rate

This varies wildly by location. Texas has high property taxes (around 2.0% to 2.5%). California has lower rates (around 1.0% to 1.2%). Your local tax assessor’s website has the exact number. If you are unsure, use 1.2% as a safe starting point.

Input Field 6: Homeowners Insurance

Budget 800to800to1,500 per year for insurance. This covers fire, theft, and liability. The FHA loan calculator divides this by 12 and adds it to your monthly payment.

Step-by-Step: Running Your First Calculation

Let us walk through a real scenario together. Meet Marcus. He lives in Phoenix, Arizona. He makes 68,000peryear.Hehas68,000peryear.Hehas14,000 saved for a down payment and closing costs. He wants to know his true budget.

Marcus opens the Free Calculator. Here is what he enters:

- Home Price: $280,000

- Down Payment: $9,800 (3.5%)

- Interest Rate: 6.25%

- Loan Term: 30 years

- Property Tax Rate: 0.85% (Maricopa County average)

- Annual Insurance: $1,200

The FHA loan calculator processes the numbers. Here is what it tells Marcus:

| Cost Component | Monthly Amount |

|---|---|

| Principal & Interest | $1,672 |

| Monthly MIP (0.55%) | $124 |

| Property Taxes | $198 |

| Homeowners Insurance | $100 |

| Total Monthly Payment | $2,094 |

Now Marcus has a reality check. His take-home pay is roughly 4,600permonth.A4,600permonth.A2,094 mortgage is 45% of his income. That is tight. He decides to look at cheaper homes.

He changes the home price to 250,000.The∗∗FHAloancalculator∗∗updatesinstantly.Newtotal:250,000.The∗∗FHAloancalculator∗∗updatesinstantly.Newtotal:1,870 per month. That is 40% of his income. Still not comfortable. He tries 230,000.Newtotal:230,000.Newtotal:1,720 per month (37% of income). Much better.

Without the FHA loan calculator, Marcus would have started shopping at $280,000 and fallen in love with a house he could not afford. That is the secret power of this tool.

How to Factor in Your Debt-to-Income Ratio

The FHA loan calculator tells you your housing payment. But lenders look at your total debt-to-income (DTI) ratio. This includes your car loan, student loans, credit card minimums, and any other monthly debt.

Here is the rule: Your total monthly debt (including the new mortgage) should not exceed 43% to 50% of your gross monthly income, depending on the lender.

Let us run an example using our FHA loan calculator results.

Scenario: Sarah earns $6,000 per month gross income.

- New mortgage payment (from calculator): $2,000

- Car payment: $400

- Student loan: $300

- Credit card minimum: $100

- Total debt: $2,800

2,800÷2,800÷6,000 = 46.7% DTI. Sarah is approved.

If Sarah’s DTI exceeded 50%, the FHA loan calculator would not catch that directly. So you must do this second step manually. Use the calculator to get the mortgage number, then add your other debts, then divide by your income.

The Secret: Testing Different Down Payments

Most people assume 3.5% is always the best choice. That is not always true. Put your numbers into the FHA loan calculator three times with different down payments. Watch what happens to your monthly MIP.

**Test 1: 3.5% down on a 250,000home∗∗(250,000home∗∗(8,750 down)

- Loan amount: $241,250

- Monthly MIP: Approximately $135

- Total payment: $1,850

**Test 2: 5% down on a 250,000home∗∗(250,000home∗∗(12,500 down)

- Loan amount: $237,500

- Monthly MIP: Approximately $109 (lower because more equity)

- Total payment: $1,790

**Test 3: 10% down on a 250,000home∗∗(250,000home∗∗(25,000 down)

- Loan amount: $225,000

- Monthly MIP: Approximately $84 (even lower)

- Total payment: $1,700

Saving an extra 16,250(toreach1016,250(toreach10150 per month forever. The FHA loan calculator shows you this trade-off clearly. Sometimes waiting six more months to save a larger down payment is the brilliant move.

Real-World Example: The $50,000 Income Trap

Let me show you a dangerous scenario that the FHA loan calculator prevents.

Jenna makes 50,000peryear.Thatisabout50,000peryear.Thatisabout4,166 per month gross. A lender pre-approves her for a $240,000 FHA loan because her credit score is 620. She is thrilled. She starts shopping.

But Jenna uses this Calculator first. She enters:

- Home Price: $240,000

- Down Payment: $8,400 (3.5%)

- Interest Rate: 6.5%

- Taxes: 1.1%

- Insurance: $1,000/year

The FHA loan calculator returns: $1,950 per month.

1,950is471,950is47800 for everything else — food, gas, utilities, car insurance, medical bills. That is a recipe for disaster.

Jenna lowers her target to 190,000.The∗∗FHAloancalculator∗∗shows190,000.The∗∗FHAloancalculator∗∗shows1,580 per month. Much safer. She finds a charming condo instead of a single-family home. She buys it comfortably.

The lender would have let Jenna ruin her life. The FHA loan calculator saved her.

Common Mistakes People Make

Mistake 1: Forgetting Closing Costs

The FHA loan calculator focuses on monthly payments. It does not include closing costs (typically 2% to 4% of the home price). On a 250,000home,closingcostsadd250,000home,closingcostsadd5,000 to $10,000 in cash needed at the table. Always add this to your savings goal.

Mistake 2: Using the Wrong Interest Rate

Rates change daily. The FHA loan calculator is only as good as the rate you enter. Check HUD’s official FHA resources for program updates, then call three lenders for actual quotes.

Mistake 3: Ignoring Utility Costs

A 2,000mortgageplus2,000mortgageplus400 in utilities is actually a 2,400housingcost.The∗∗FHAloancalculator∗∗cannotpredictyourelectricbill.Add2,400housingcost.The∗∗FHAloancalculator∗∗cannotpredictyourelectricbill.Add200 to $400 to your calculator result for a true “total shelter cost.”

How to Use the Calculator with a Real Estate Agent

Walk into your first agent meeting with printed results from your FHA loan calculator. Hand it to the agent. Say, “I have already run my numbers. My maximum comfortable monthly payment is 2,200.Basedoncurrentratesandtaxes,thatmeansmymaximumhomepriceisapproximately2,200.Basedoncurrentratesandtaxes,thatmeansmymaximumhomepriceisapproximately290,000. Please only show me homes under $290,000.”

The agent will respect you immediately. You are not a tire-kicker. You are a serious buyer with a budget. The FHA loan calculator gives you credibility and saves everyone time.

Advanced Feature: The Amortization Schedule

A great FHA loan calculator includes an amortization schedule. This is a table showing every single payment for 360 months. It tells you:

- How much of each payment goes to interest (high at the start)

- How much goes to principal (low at the start)

- When you cross the 20% equity threshold

Why does this matter? Because once you have 20% equity, you can refinance out of the FHA loan into a conventional loan and drop MIP forever. The amortization schedule from your FHA loan calculator shows you exactly which month that happens.

For example, on a $250,000 loan at 6% interest, you hit 20% equity around month 90 (year 7.5). Now you have a target date. Seven and a half years until you can drop MIP. That is actionable information.

Conclusion: Stop Guessing, Start Calculating

Homebuying is stressful enough without financial surprises. You should never sign a mortgage contract without first running every single scenario through a reliable tool. The FHA loan calculator is not optional. It is essential.

We have covered:

- Why generic calculators fail FHA buyers

- How to enter every input field correctly

- Real-world examples that prevent costly mistakes

- How to calculate your true DTI

- The secret power of testing different down payments

Now you have the knowledge. The only thing missing is action.

Your Call to Action:

Open FHA Calculator right now. Run three scenarios:

- Your dream home price

- Your conservative home price

- Your “stretch but possible” home price

Compare the monthly payments. Look at the MIP costs. Check the amortization table. Then call one lender and ask for a real rate quote. Plug that rate back into the FHA loan calculator. Adjust your search range accordingly.

Then share this article with a friend who is house hunting. They need this tool more than you know. The FHA loan calculator is free, fast, and could save them thousands of dollars and years of financial stress.

Do not be Marcus before the calculator. Be Marcus after the calculator. Know your numbers. Buy with confidence. Sleep well at night.