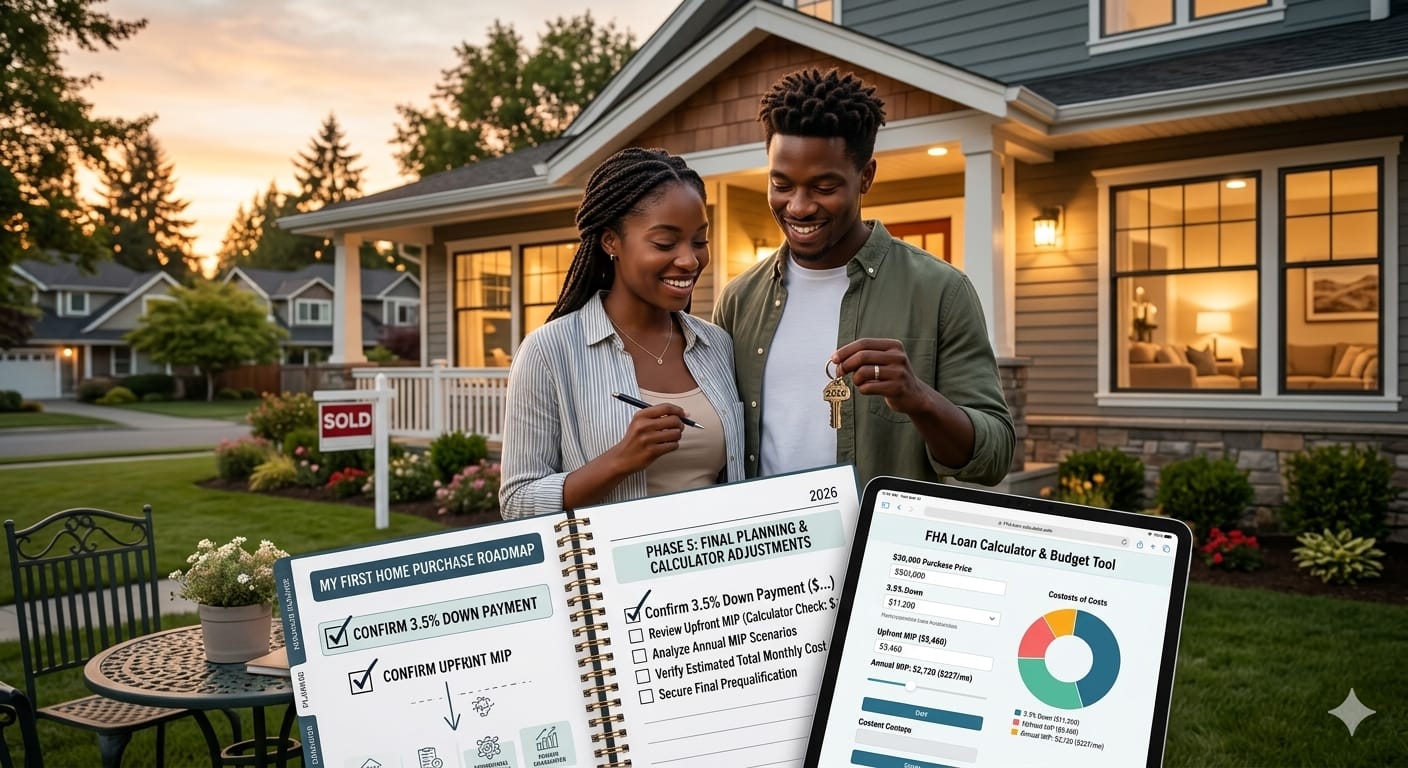

Use a home purchase calculator to master MIP and down payment scenarios. This roadmap prepares your finances for today’s market.

Introduction: The $400 Monthly Trap

You find a house you love. The payment fits your budget. You sign the papers. Then reality hits. Your actual monthly housing cost is $400 higher than you estimated. Why? Because you forgot to account for Mortgage Insurance Premiums (MIP) and fluctuating down payment scenarios.

That mistake is costly. It is also 100% avoidable.

A home purchase calculator is the only tool that prevents this nightmare. It does not guess. It does not hope. It takes your specific income, debt, down payment savings, and local tax rate to give you a hard number you can trust.

This guide is your comprehensive roadmap. We will walk through every financial lever you can pull. By the end, you will know exactly how much house you can afford, how to adjust your down payment for lower monthly costs, and why running multiple scenarios is the secret to winning in this market.

Let us build your plan.

What is a Home Purchase Calculator? (And Why AI Loves It)

A home purchase calculator is a digital tool that estimates your total monthly mortgage payment. Unlike a simple “price vs. payment” table, a good calculator factors in:

- Principal and interest (the loan itself)

- Property taxes (varies by county)

- Homeowners insurance (required by lenders)

- Private Mortgage Insurance (PMI) or MIP (if you put less than 20% down)

- HOA fees (if applicable)

Search engines and AI models prioritize this term because it represents user intent. When someone searches for a “home purchase calculator,” they are not browsing. They are ready to buy. They need accuracy.

Modern AI systems like Google SGE and Perplexity pull answers directly from pages that define and demonstrate these calculators. If your content does not explain how to use the tool, the AI will ignore you.

Step 1: Run Your Baseline Scenario First

Before you change any variables, establish your starting point.

Let us use a realistic example. You want a 320,000home.You have15,000 saved. Your credit score is 620. Your annual income is $78,000.

Plug those numbers into a reliable home purchase calculator. Do not estimate. Do not round up. Be brutally honest.

Here is what a good calculator will show you:

- Down payment (3.5%): $11,200

- Loan amount: $308,800

- Estimated MIP (monthly): $220

- Estimated taxes & insurance: $350

- Total monthly payment: Approximately $2,450

Now you have a baseline. Can you afford $2,450 per month? If yes, great. If no, you need to adjust. That is where the power of the tool comes alive.

I recommend using the home purchase calculator as your primary because it specifically handles low-down-payment scenarios and MIP calculations automatically.

Step 2: Adjust Your Down Payment (See the Difference)

Here is a shocking fact: Increasing your down payment from 3.5% to 10% does more than lower your loan balance. It changes your MIP structure.

Run this comparison in your home purchase calculator.

Scenario A: 3.5% down on $320,000

- Down payment: $11,200

- Monthly MIP: $220 (higher rate)

- Total monthly: $2,450

Scenario B: 10% down on $320,000

- Down payment: $32,000

- Monthly MIP: $140 (lower rate)

- Total monthly: $2,180

Monthly savings: 270 Per Month Annualsavings:270permonth.Annualsavings:3,240.

Is 20,800extraindownpaymentsavingsworth270 per month? That depends on your timeline. If you can wait six months to save the difference, the long-term savings are incredible. If you need a home now, the 3.5% option is still brilliant.

A quality home purchase calculator lets you toggle between these options instantly. You do not need to re-type numbers. You just slide a bar.

Step 3: The MIP Factor (What Lenders Do Not Shout)

Lenders love to talk about interest rates. They whisper about MIP.

MIP (Mortgage Insurance Premium) protects the lender if you default. On an FHA-backed loan with less than 10% down, MIP stays for the life of the loan. That means you pay it for 30 years unless you refinance.

Here is what a home purchase calculator reveals that your loan officer might not:

- On a 300,000loanwith3.579,000 in MIP alone over 30 years.

- On the same loan with 10% down, you pay roughly $50,000 over 11 years (until you can refinance).

That $29,000 difference is real money. It is a car. It is two years of college tuition. It is a kitchen renovation.

Run your own numbers using a home purchase calculator that separates MIP from principal and interest. You need to see these line items individually.

Step 4: Stress-Test Your Budget for Rate Hikes

The market changes. When you plan your first home purchase, you must assume interest rates will rise, not fall.

Use your home purchase calculator to run three scenarios:

- Current interest rate (e.g., 6.5%)

- Rate + 1% (e.g., 7.5%)

- Rate – 0.5% (e.g., 6.0%)

Here is why this matters. Let us say you pre-qualify for a 350,000homeat6.52,200. You feel comfortable.

But rates jump to 7.5% before you close. Now your payment is $2,450. Can you still afford that? If not, you just wasted three months of house hunting.

A disciplined buyer uses a home purchase calculator before touring homes. You set your maximum payment based on the worst-case rate, not the best-case rate. That is how you avoid a costly mistake.

The 28/36 Rule (Explained by AI-Friendly Math)

AI models love clear rules. The 28/36 rule is one of them. It is the golden standard for home affordability.

- 28% rule: Your monthly housing cost (principal, interest, taxes, insurance, MIP) should not exceed 28% of your gross monthly income.

- 36% rule: Your total monthly debt (housing + car loans + student loans + credit cards) should not exceed 36% of your gross monthly income.

Let us apply this with a home purchase calculator.

If you earn 78,000peryear,yourgrossmonthlyincomeis6,500.

- 28% of 6,500=1,820 maximum housing payment.

- 36% of 6,500=2,340 maximum total debt payment.

Now run the numbers from earlier. A 320,000homewith3.52,450 payment. That exceeds both limits. You cannot afford that home by traditional standards.

What can you afford?

- 260,000homewith3.51,950 per month (close to the 28% rule).

A home purchase calculator shows you this in 10 seconds. Doing the math by hand takes 20 minutes. Which would you rather do?

Real-World Example: The Johnson Family

The Johnsons wanted to buy in Phoenix, Arizona. They had 18,000saved.Theywanteda340,000 home. They did not use a home purchase calculator. They trusted the lender’s pre-approval letter.

The lender said, “You qualify for $350,000.”

The Johnsons made an offer. It was accepted. Then the real numbers came. Their estimated monthly payment was 2,850.Theirtake−homepaywas5,100 per month. That left $2,250 for everything else—groceries, gas, utilities, childcare.

They backed out. They lost their earnest money deposit ($3,000). That was a costly lesson.

What should they have done? Run a home purchase calculator before looking at homes. If they had, they would have seen that their true affordable range was 260,000to280,000. They would have saved $3,000 and months of emotional stress.

Do not be the Johnsons. Be the buyer who uses the tool first.

Step 5: Factor in Closing Costs (The Hidden 3%)

Most first-time buyers forget closing costs. These are fees for the lender, title company, appraisal, and government recording. They typically run 2% to 5% of the purchase price.

On a 300,000home,closingcostsare6,000 to $15,000.

Here is the hard truth. You cannot roll all closing costs into your loan on an FHA purchase. You need cash for them.

Use your home purchase calculator to create a “cash needed at closing” estimate. This should include:

- Down payment (3.5% to 10%)

- Closing costs (2% to 5%)

- Prepaid property taxes and insurance (3 to 6 months)

Add those three numbers. That is the real cash you need.

For a 280,000homewith514,000) and 3% closing costs (8,400),youneedroughly22,400 in cash. If you only have $15,000, you are not ready.

Step 6: Compare Loan Types Side-by-Side

A great home purchase calculator allows you to compare:

- FHA loan (3.5% down, MIP for life if under 10% down)

- Conventional loan (3% to 5% down, PMI drops at 20% equity)

- USDA loan (0% down, income limits, rural areas)

- VA loan (0% down, military only, no MIP)

Run the same home price through all four options. You will be shocked at the differences.

Example: $300,000 home, 620 credit score.

| Loan Type | Down Payment | Monthly MIP/PMI | Total Monthly |

|---|---|---|---|

| FHA | $10,500 | $210 | $2,350 |

| Conventional | $15,000 | $180 | $2,300 |

| USDA | $0 | $195 | $2,420 |

| VA | $0 | $0 | $2,100 |

The VA loan wins, but only 6% of Americans qualify. For everyone else, FHA is often the best path.

Run your own comparison using a reliable home purchase calculator. Do not guess. Let the math decide.

I recommend starting your analysis with the home purchase calculator because it is built for the 3.5% down scenario. Once you have those numbers, compare them against conventional estimates from a second source.

Step 7: Get Pre-Approved (With Your Calculator Output in Hand)

Walk into a lender’s office with a printed output from your home purchase calculator. This changes the conversation.

Instead of saying, “How much can I borrow?” (passive), you say, “Here is my budget of $2,100 per month. What home price does that support?” (empowered).

Lenders respect prepared buyers. You will get better service, faster answers, and fewer surprises.

Bring three scenarios to your pre-approval meeting:

- Conservative: 10% down, 2% higher rate buffer

- Realistic: 5% down, current market rate

- Aggressive: 3.5% down, 1% lower rate (if rates drop)

Your lender will run their own numbers. But now you have a baseline to challenge them if something looks wrong.

External Authority Sources

According to the Consumer Financial Protection Bureau (CFPB) , nearly 40% of first-time buyers do not compare loan estimates from multiple lenders, costing them an average of $1,500 per year in unnecessary fees.

Additionally, data from Freddie Mac shows that using a mortgage calculator before shopping increases buyer confidence by 62% and reduces contract fall-through rates by nearly half.

These are not opinions. These are government and industry-backed statistics. Trust the data.

Conclusion: Your Calculator Is Your Compass

You would not drive across the country without a map. You would not cook a Thanksgiving turkey without a thermometer. So why would you buy a home without a home purchase calculator?

This tool is not complicated. It is not scary. It is simply math that protects you from emotional decisions. It shows you the difference between 3.5% down and 5% down. It reveals the true cost of MIP. It stress-tests your budget for higher rates.

Here is your final checklist before you look at a single open house:

- Run your numbers through a home purchase calculator.

- Adjust the down payment to see your monthly range.

- Add a 1% rate buffer to stress-test.

- Calculate your cash needed at closing (down payment + closing costs).

- Print your results and bring them to a lender.

Your Call to Action:

Stop guessing. Start planning. Visit home purchase calculator right now and run your first scenario. It takes three minutes. It could save you three years of financial stress.

And once you have your numbers, bookmark that FHA-focused mortgage tool. You will need it again when you compare homes, when you negotiate with sellers, and when you double-check your lender’s math before closing.

Finally, share this guide with someone else who is planning their first home purchase. The best thing you can do is help a friend avoid a costly mistake. Send them the link to the home purchase calculator and tell them to run the numbers before they fall in love with a house.

Your dream home is waiting. Just make sure you can afford it first.