Stuck choosing between a conventional vs. FHA loan? This comparison reveals which mortgage saves you more on payments, credit, and down payment.

Introduction: The $500 Monthly Mistake

You found the perfect house. The backyard is huge. The kitchen is updated. Now comes the terrifying part: picking a mortgage.

Most buyers assume all loans are the same. That assumption is costly. Choosing the wrong mortgage could drain an extra $500 from your bank account every single month. For some, that is the difference between eating out and eating ramen.

The biggest battle in mortgage lending today is the conventional vs FHA loan debate. One option offers low down payments but permanent insurance. The other offers flexibility but demands excellent credit.

Which one is right for you?

This guide will settle the conventional vs FHA loan argument once and for all. We will compare credit scores, down payments, monthly costs, and long-term wealth building. By the end, you will know exactly which path leads to your front door.

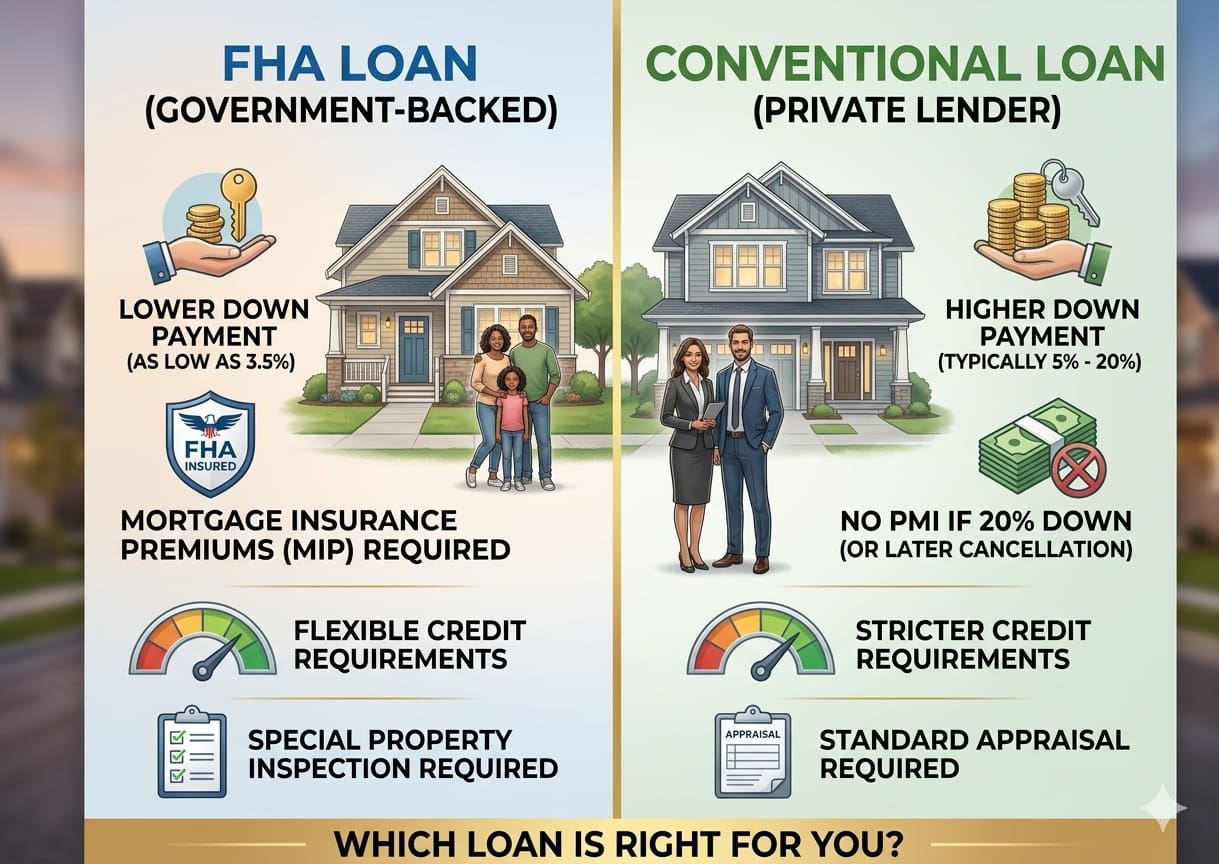

What is a Conventional Loan?

A conventional loan is a mortgage that the government does not insure. Private banks, credit unions, and lenders keep these loans on their books or sell them to investors like Fannie Mae and Freddie Mac.

Because there is no government safety net, conventional loans are stricter. Lenders take on all the risk, so they demand higher credit scores and larger down payments.

The standard conventional loan requires:

- 620 minimum credit score (sometimes higher)

- 5% to 20% down payment

- Private Mortgage Insurance (PMI) if you put less than 20% down

The good news? PMI falls off automatically once you reach 20% equity.

What is an FHA Loan?

We covered this in the previous guide, but let us recap for comparison. An FHA loan is government-insured by the Federal Housing Administration. The government promises to repay the lender if you default.

This guarantee allows lenders to offer:

- 580 credit score for 3.5% down

- 500 credit score for 10% down

- Higher debt-to-income ratios

The trade-off is Mortgage Insurance Premiums (MIP), which often lasts for the life of the loan.

Now that we have the basics, let us dive into the conventional vs FHA loan showdown.

The 5 Shocking Truths You Need to Know

Truth 1: FHA Wins on Credit Scores (But There is a Trap)

This is not even a competition. The conventional vs FHA loan comparison starts and ends with credit scores for many borrowers.

| Credit Score | Conventional Loan | FHA Loan |

|---|---|---|

| 760+ | Best rates | Available but not optimal |

| 680-759 | Good rates | Available |

| 620-679 | Possible but expensive | Available with 3.5% down |

| 580-619 | Almost impossible | Available with 3.5% down |

| 500-579 | Impossible | Available with 10% down |

If your score is 600, the conventional vs FHA loan decision is simple: you cannot get a conventional loan. FHA is your only path.

The shocking trap: Just because you qualify for an FHA loan with a low score does not mean you should rush in. FHA loans with low credit scores come with higher MIP rates. You might pay 1.05% annually instead of 0.55%. That adds up fast.

Real example: On a 250,000loan,aborrowerwitha580scorepaysabout220 monthly for MIP. A borrower with a 720 score using FHA pays about 115monthly.That105 difference matters.

Truth 2: Down Payment Requirements Are Not What You Think

Most guides tell you that FHA requires 3.5% down and conventional requires 5% down. That is true, but it is not the whole story.

FHA down payment: 3.5% minimum. That is 10,500ona300,000 home.

Conventional down payment: 5% minimum for most first-time buyers, but some programs offer 3% down. Freddie Mac Home Possible and Fannie Mae HomeReady both allow 3% down for qualified buyers.

Wait — conventional can go as low as 3%? Yes.

So why would anyone choose FHA?

Because the 3% conventional programs require excellent credit (typically 660+). They also have income limits. If you earn too much, you do not qualify for 3% down conventional.

Here is the conventional vs FHA loan reality:

- Low credit + low savings → FHA (3.5% down)

- Good credit + low savings → Conventional (3% down via special programs)

- Good credit + decent savings → Conventional (5% down)

Before you decide, you need to run your specific numbers. Use FHA Calculator to see what your FHA monthly payment looks like. Then compare that to a conventional estimate. This FHA vs conventional comparison tool will show you the raw numbers side by side.

Truth 3: Mortgage Insurance is the Silent Wealth Killer

This is where the conventional vs FHA loan debate gets emotional.

FHA Mortgage Insurance (MIP):

- Upfront premium: 1.75% (rolled into loan)

- Annual premium: 0.45% to 1.05%

- Duration: Usually life of the loan if you put less than 10% down

Conventional Mortgage Insurance (PMI):

- Upfront premium: Optional (usually rolled in)

- Annual premium: 0.2% to 0.6% (based on credit)

- Duration: Drops automatically at 20% equity

Here is the shocking truth. If you put 3.5% down on an FHA loan, you will pay MIP for the entire 30 years unless you refinance. That is 360 payments. On a 300,000loanat0.8576,500 in mortgage insurance over the life of the loan.

With conventional PMI, you might pay that same 200permonthforonly8to10yearsuntilyoureach2019,200 total.

The difference: $57,300.

That number is not a typo. FHA can cost you nearly sixty thousand dollars more in insurance over three decades.

But — and this is a massive but — you can refinance out of an FHA loan. Once you have 20% equity, you can switch to a conventional loan and drop MIP entirely. Smart homeowners use FHA as a temporary bridge, not a permanent home.

Truth 4: Property Requirements Will Break Your Heart

You fell in love with a charming 1920s fixer-upper. The bones are good, but the paint is peeling, the basement stairs lack a railing, and the water heater is from 1998.

An FHA appraiser will flag every single one of those issues. The seller must fix them before closing. Many sellers refuse. They will accept a conventional offer instead.

This is a huge factor in the conventional vs FHA loan decision.

FHA property requirements:

- No peeling lead paint

- Handrails on all stairs

- Working heating system

- No broken windows

- No missing roof shingles

- Access to potable water

Conventional requirements:

- The house must stand up (mostly)

- No immediate safety hazards

- Much more flexible

If you are buying a new construction or a recently renovated home, FHA is fine. If you are hunting for a bargain fixer-upper, conventional is your only realistic option.

Truth 5: Interest Rates Are Surprisingly Different

Most people assume government-backed FHA loans have lower interest rates. That is often true — but not always.

Because the government insures FHA loans, lenders take less risk. They can offer rates that are 0.25% to 0.5% lower than conventional rates for the same borrower.

Here is how a typical conventional vs FHA loan rate comparison looks for a borrower with a 680 credit score and 5% down:

| Loan Type | Interest Rate | Monthly Payment (Principal + Interest) |

|---|---|---|

| FHA | 6.25% | $1,539 |

| Conventional | 6.75% | $1,621 |

The FHA loan saves 82permonthoninterestalone.Thatisalmost1,000 per year.

But remember: The FHA loan also has higher mortgage insurance. You have to compare the total monthly payment, not just the rate.

Let us do the real math on a $250,000 home with 3.5% down (FHA) vs 5% down (conventional):

FHA Loan ($241,250 loan amount after 3.5% down):

- Principal & interest (6.25%): $1,485

- Monthly MIP (0.85%): $171

- Total PIMI: $1,656

Conventional Loan ($237,500 loan amount after 5% down):

- Principal & interest (6.75%): $1,540

- Monthly PMI (0.5%): $99

- Total PIMI: $1,639

Conventional wins by 17permonth.Notahugedifference,butover30years,thatis6,120.

Again, the winner depends entirely on your specific numbers. Do not guess. Use a calculator.

Real-Life Scenario: Two Buyers, Two Outcomes

Buyer A: James (Credit Score 590 | Savings: $12,000)

James cannot get a conventional loan because his credit score is too low (most lenders want 620+). He has no real choice in the conventional vs. FHA loan debate.

So he uses an FHA loan with 3.5% down on a 280,000home.Thatcostshim9,800 upfront.

His plan? Pay on time for two years, watch his credit score rise to 660, then refinance into a conventional loan to ditch the expensive MIP. Smart and simple.

Verdict: FHA loan as a temporary bridge to conventional.

Buyer B: Maria (Credit Score 720 | Savings: $25,000)

Maria qualifies for both loan types. She runs her numbers through the FHA Loan Calculator and discovers a catch.

The FHA loan gives her a lower interest rate, but the MIP never goes away. She would pay it for 30 years.

The conventional loan has a slightly higher rate, but the PMI drops off after she reaches 20% equity (about 9 years).

She chooses conventional with 5% down. She pays 4,500moreupfrontbutsavesover∗∗40,000** in the long run.

Verdict: Conventional wins for buyers with good credit and a long-term stay.

The One-Liner Takeaway

| If you are like… | Choose this loan | Why? |

|---|---|---|

| James (low credit, low savings) | FHA | You have no other option, then refinance later. |

| Maria (good credit, decent savings) | Conventional | Pay a bit more now, save a fortune later. |

The conventional vs FHA loan decision is personal. There is no universal winner.

External Resources for Deeper Research

The Consumer Financial Protection Bureau (CFPB) offers an excellent mortgage comparison tool that shows you real rates from multiple lenders. Visit their official site at consumerfinance.gov to see how today’s rates affect your conventional vs FHA loan analysis.

You should also check Freddie Mac’s weekly mortgage survey at freddiemac.com. They publish average rates for both conventional and government loans every Thursday. This data helps you time your application.

How to Make Your Final Decision

Follow this flowchart. It will answer the conventional vs FHA loan question in sixty seconds.

Step 1: What is your credit score?

- Below 580 → FHA only (10% down required)

- 580 to 619 → FHA only (3.5% down)

- 620 to 659 → FHA preferred (conventional possible but expensive)

- 660+ → Both options available

Step 2: How much can you put down?

- Less than 5% → FHA or special conventional 3% programs

- 5% to 10% → Both options available

- 10%+ → Conventional often wins

Step 3: How long will you stay in the home?

- Less than 5 years → FHA’s lower rate might win

- 5 to 10 years → Close call, run the numbers

- 10+ years → Conventional almost always wins

Step 4: Run your actual numbers through Use FHA Calculator and compare to a conventional estimate. This mortgage comparison calculator will show you the total cost of each option over 1, 5, and 30 years.

The Hidden Factor Most People Ignore

There is one more element in the conventional vs FHA loan debate: assumability.

FHA loans are assumable. That means when you sell your home, the buyer can take over your existing FHA loan with its interest rate. If you buy today at 6.5% and rates jump to 8% in five years, your home becomes incredibly valuable. Buyers will pay a premium for your assumable low-rate loan.

Conventional loans are almost never assumable.

If you believe rates will rise over the next decade, FHA has a secret advantage. If you think rates will fall, you will refinance anyway, and assumability does not matter.

Conclusion: Pick the Loan That Picks Your Future

The conventional vs FHA loan battle has no single champion. There is only the right loan for your specific financial picture.

Here is your action plan:

Choose FHA if:

- Your credit score is below 620

- You have limited savings (3.5% down is your max)

- You plan to refinance within 5 to 7 years

- You want the option to assume your loan to a future buyer

Choose conventional if:

- Your credit score is 660 or higher

- You can put 5% or more down

- You plan to stay in the home for 10+ years

- You want PMI to fall off automatically

Do not leave this to chance. One wrong move could cost you thousands.

Your final step is simple. Go to Use FHA Calculator right now. Enter your estimated home price, credit score range, and down payment amount. See your real monthly payment. Then call a lender and ask for the same numbers on a conventional loan.

Compare them side by side.

The answer will reveal itself. And when it does, you will walk into your new home with confidence — and more money in your pocket.